DoorDash’s IPO: A Breakdown of its S-1

Will it continue to deliver? Chew on this 10 minute read.

Written over miso soup & spicy tuna rolls that were, fittingly, DoorDashed.

DoorDash’s S-1 dropped a few days ago. After reading through its 250+ pages, it’s clear that there is an arms race in the brick & mortar delivery space. From one of most comprehensive S-1’s I’ve seen including details on unit economics, cohort behavior, and KPIs, I’ll be breaking down the #dash to be the top dog in this expanding, yet competitive, marketplace that faces no shortage of macro uncertainties. When tech, along with consumer demand for convenience and omnichannel experience, turn the physical world into new marketplaces, new frontiers and challenges inevitably arise in new ways.

1 min TL;DR. Perfect for (Zoom) happy hours.

State of the Union

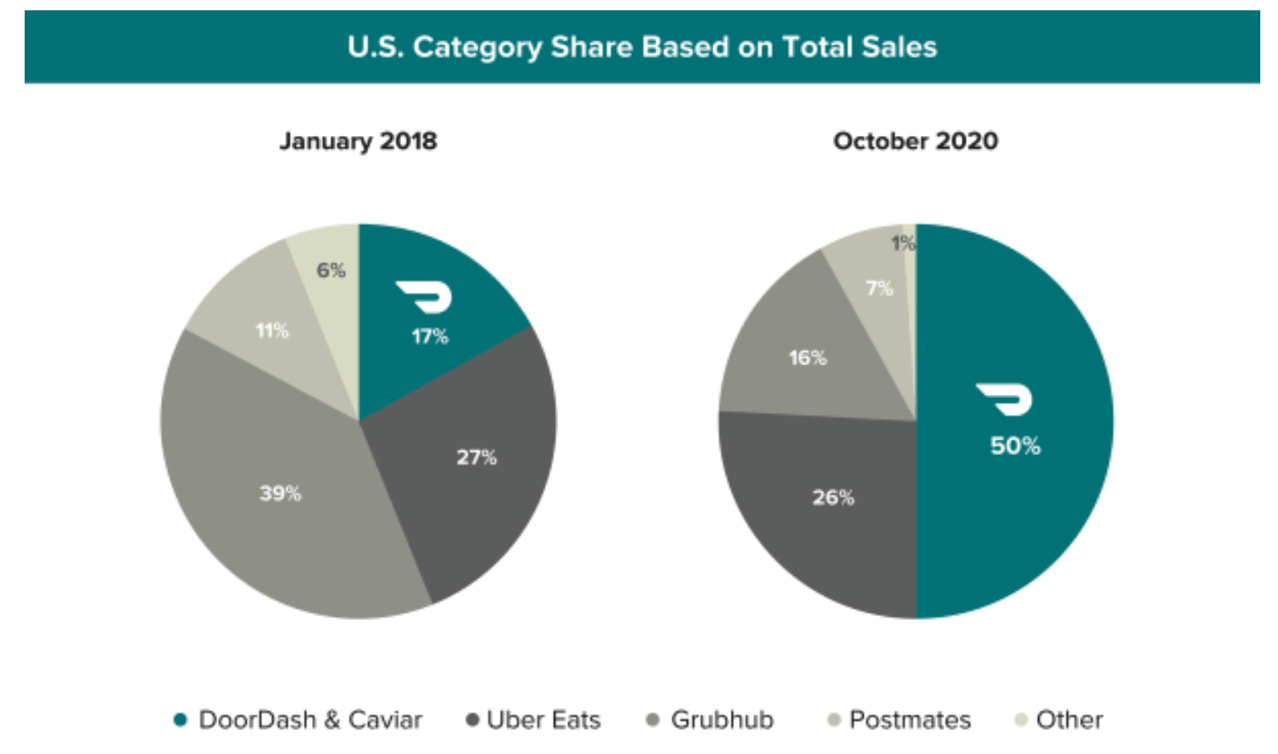

In the last 2.5 years, DoorDash has emerged as the biggest contender in the food delivery space with 50% of the market share. Uber and Grubhub have 33% and 16%, respectively

DoorDash has the unit economics, balance sheet, and network effects from (1) its logistics system, (2) merchants, and (3) customers to keep its lead

The brick & mortar delivery marketplace has a lot of room to grow

However, the competition in this marketplace is fierce amongst not just these three giants (Dash, Uber, & Grubhub), but also Amazon, retailers’ propriety ordering systems, and specialized cuisine apps like Slice

The future is not clear on many fronts among which are gig economy supply & regulations like CA’s Prop 22, post COVID times, international laws, true TAM (total addressable market), and differences in the restaurant versus other brick & mortar delivery business economics

Fun cocktail tidbit - while S-1s and SEC filings contain a “risks” section, DoorDash’s is hefty. “Risks” go from page 22 to page 80

Company Snapshot

Founded in 2013 and based in SF. Now operates in the US, Canada, & Australia

Its mission is to help local brick & mortar businesses compete, succeed, & flourish in line with consumer demand for convenience and omnichannel experience

390k merchants

18M customers

1M Dashers

900M orders since 2013

$32 average order value

35 min average delivery time

9 min deep dive. Chicago pizza style.

DoorDash as a Company

Even longtime naysayers (something DoorDash has had no shortage of since its inception in 2013, e.g., Techcrunch, NYT, WSJ) would be hard-pressed to deny that DoorDash has, ahem, delivered as a business.

The positives:

It’s the biggest player in the market

Today, it has 50% of the total food delivery service market. In suburban markets alone, it is at 58%. In 2019, it acquired Caviar from Square for $410M. $310M was in cash and the remaining $100M in convertible preferred stock

It’s had insane growth in a short time with improving underlying economics

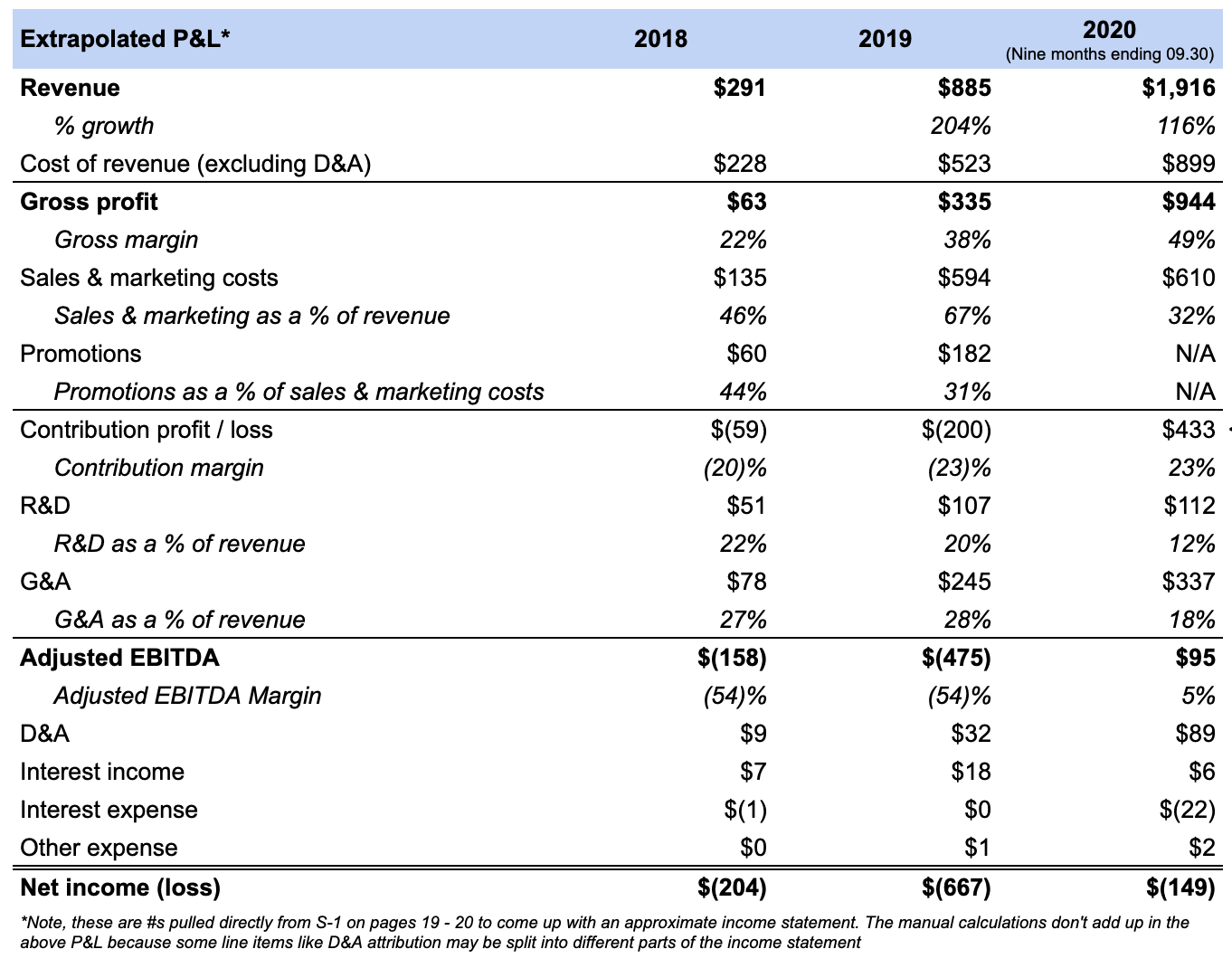

As recently as Jan 2018, its market share was 17% compared to the current 50%. As seen from my extrapolated P&L (pieced together from various financials throughout the S-1), year-over-year revenue growth has seen 1.5 to 2x since 2018. Despite spending heavily to acquire new customers, it’s now contribution profit and EBITDA positive. Gross margins have increased to almost 50% while sales & marketing spend relative to revenue has decreased

It successfully acquires & retains merchants

DoorDash has 390k merchants and partnership with 82% of the 200 major restaurant groups because it knows how to add incremental volume for merchants by increasing # of orders and average order value. Using analytics & economics of scale, Dash can offer services ranging from pricing and menu determination to a whitelabel logistics solution called DoorDash Drive. Plus, in an industry where merchants are charged 15% - 30%, DoorDash charges 18%. See below for my units economics breakdown:

It successfully acquires & retains customers

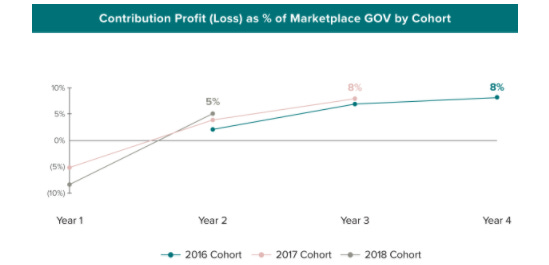

Customer cohort economics were one of the best surprises that Dash shared. While customer cohorts are net revenue negative in year 1, cohorts become LTV / CAC positive (roughly 3:1) as spend increases each subsequent year. As a result, promotions and marketing spend focus on customers in year 1 to increase their usage and instill a habit of ordering DoorDash.

Superior customer experience for each transaction, discounts, and the loyalty program DashPass (~5M members strong) are just some of the ways Dash ensures this.

It manages a complex logistics system that makes work attractive to gig workers

1M Dashers and other infrastructure investment Dash has made, has enabled Dash to have a 35 minute average delivery timeIts growth shows a powerful flywheel effect at play

Dash created a way to build brand and generate network effects between their 3 symbiotic pillars of merchants, Dashers, and customers. It has, as Lenny Rachitsky calls it, magical growth loops

It’s got the cash and P&L

Despite heavy marketing spend (32% of revenue for 2020), Dash has the liquidity to grow. Additionally, its revenue, sales & marketing spend, contribution profit (loss), and EBITDA make a solid case for underlying economics as it continues to scale

It’s got the team

From its S-1’s numbers about its growth rate, market share, and focus on the right metrics, it’s evident the company is well-steered. Helming this growth is a young, hungry founding team (ages 36, 28, and 27). Bonus: in the appendix, scroll to see how ownership and voting share break down in the cap table)

Some cautionary tales:

There’s no visibility to DoorDash’s pre-2018 numbers

Because of the JOBS Act of 2012, DoorDash is not obligated to report more than 2 years of earnings. Therefore, while recent growth is laud worthy, the lack of past growth trends make it even harder to calibrate when evaluating future growths in a nascent marketplaceThis IPO’s fiscal structure is a bit atypical

Two things: first, there is no dividend issuance plan. Second, unlike in typical IPOs, DoorDash has not given the underwriters the option to purchase additional Class A shares at the IPO price - while this likely shows management’s confidence in Dash, prospects, the trading prices may be more volatileDoorDash is IPO-ing during a time of record-high COVID cases

markets are volatile despite the promise of two new vaccines

DoorDash Relative to the Macro Environment

The heavyweight competitors and lack of clarity into what long term business dynamics will be, make divining this marketplace’s future as clear as the Golden Gate Bridge on a foggy SF morning.

On the bright side, there is more pie for everyone in this market. In 2019, Americans spent $600B in restaurants. About 50% of this is spent off-premise on takeaway and delivery. The food delivery ecosystem today accounts for just 6%. Yet, how big will the pie truly get? While 6% sounds like there’s lots of room to go, the true total addressable market is unclear. After all, “only” ⅔ of Americans shop on Amazon while only 35% are Prime members.

Then there’s the eat-your-lunch-money part of this market,

Competition is immense from giants in the food delivery space and adjacent competitors competing for the brick & mortar delivery space

(A) The food delivery space with UberEats and Grubhub

With rides declining during COVID times (Uber’s Q1 results here, Q2 results here), Uber is especially focused on food delivery. Just this year, it acquired Postmates for $2.65B. Grubhub has been losing market share but was recently acquired by Just Eat Takeaway.com for $7.3B

(B) Other delivery competitors

Food delivery services know more pie is to be had by expanding to all types of brick & mortar businesses. This runs DoorDash and co. up against titans like Amazon, Shipt, and Instacart

(C) Proprietary restaurants’ ordering platforms

As technology becomes more table stakes, ultimately marketplaces serve as middlemen. Companies like Domino’s have, and continue to, develop their own tech-enabled ordering platforms

(d) New specialized entrants

With all cuisines available, customers want the best in a particular field. For example, Slice specializes in only pizza deliveriesHigh, continual cash spend makes profitability a far-off reality -

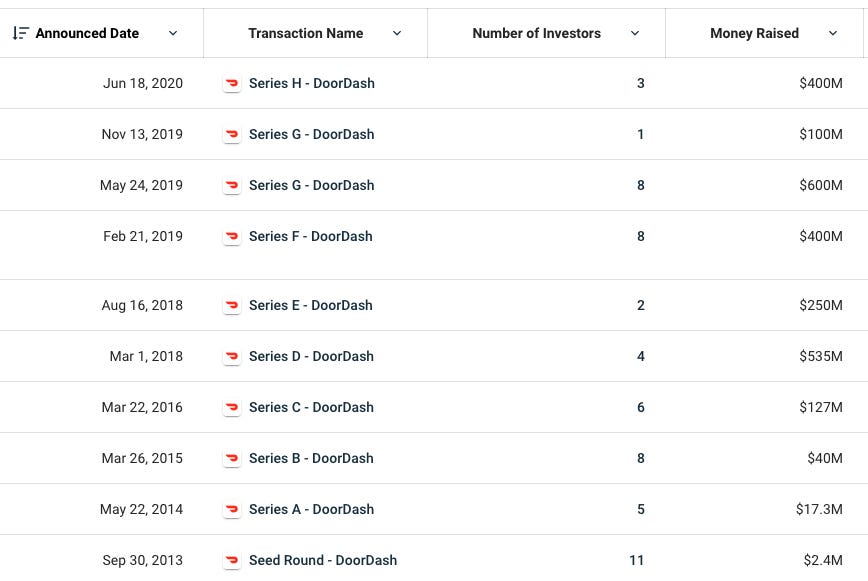

Eventually, the total market and market share available to all players will shrink. Therefore, it’s a costly arms race - it’s all about acquiring & retaining customers, investing in infrastructure and R&D in new markets, and attracting & retaining merchants. Case in point, Dash raised another $400M this summer bringing its total to $2.5B. Round information from Crunchbase:

Merchants and customers could be adversely affected in today’s COVID world -

While orders are increasing Q/Q, overall customers have less disposable income and of the 30M small businesses in the US today, many have closed or are struggling. COVID has shifted trends in favor of food delivery, but it’s unsure if this will continue as COVID times continue

Post COVID, this space faces unknowns -

(A) Customer behavior post COVID is unknown

Food delivery adoption has increased but what will happen when restaurants reopen and people are able to have in-person experiences.

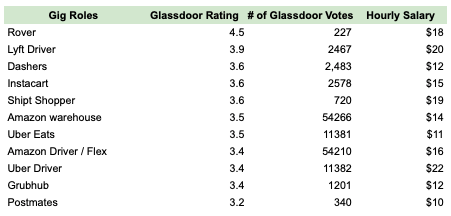

(B) Gig economy supply & regulations

Below, I compiled the top gig workers’ comps and happiness ratings. DoorDash is high on gig worker Glassdoor ratings, but low in comparison to wages. As the gig economy continues to expand, DoorDash relies heavily on its ability to attract good talent for cost-efficient prices. The story is even more uncertain if laws changes the classification of these workers to employees like CA’s Prop 22 attempted to do

The critical growth areas are largely untested -

(A) Other brick & mortar business economics

Strategy wise: it’s a smart move to go after all brick & mortar deliveries as this increases the total addressable market. Execution wise: the costs, required lift, and industry specific obstacles may cause growth to be much slower

(B) International expansion uncertainties

Cost of doing business, regulations, local competition, and the relevance of using the US’ playbook to scale are all unknowns

(C) Large metropolitan areas

DoorDash started with a focus on suburban markets and smaller cities. For Dashers, there was less traffic and easier parking. For DoorDash, average order values were higher as people generally ordered for families. For merchants, discoverability and tech savviness was an issue. For customers, time was scarce when caring for families. The transition to large metropolitan areas is like the transition to Yankee Stadium from the local park field - same concept, whole other ball game

Appendix: Shares, Equity, & Voting Rights

IPO shares outstanding

253M shares of Class A (excluding exercisable options). 31M share of Class B (excluding outstanding RSUs)[Updated] Opening price

$102 / share for a $39B valuation. The last private valuation ($16B) happened this past summer 2020. In fall 2018, there was a tender offer of 7.3M shares at $8.40 to $9.60 per share. There’s been 4 rounds raised since3 classes of shares called A, B, and C

Identical except for voting rights (A = one vote for each share, B = 20 votes for each share. Convertible to one share of A at any time, C = 0 votes for each share)Ownership & voting rights

* Financial disclaimer: On all investments, please do your own research. I am not a financial advisor and am just sharing my perspective.

Hi Shelley. Came across your page on my substack; loved the doordash summary. It was insightful, cautious yet intriguing. Looking forward to more insight breakdowns on S1s.

Love it! Interested in a 2023 revaluation.