Affirm is going public. Honest financing 'pays' off

Its S-1 'affirms' that the company is shaking up traditional credit. It's a "buy" for me.

Overview:

Ho ho ho! ‘Tis the season for big-name IPOs. Prior to going public, a company must publish a 300+ report called an S-1. And after delving into the recent flurry of S-1’s, I am excited and bullish about Affirm’s upcoming public offering:

(1) I believe in its mission to deliver honest, financial products.

(2) I’m a former employee, aka an “Affirmer''. I can attest firsthand to the passion and talent of the employees who make this mission possible.

(3) The company’s growth, plus the white space in the market, signals a very merry & lucrative future.

There are fierce competitors in this space, particularly Klarna & Afterpay. One could argue that all three are worth placing bets on, given how much white space there is. Yet, Affirm holds its own - its unique product offerings help people spend and save responsibly. So, to round out the holiday analogy, Affirm truly ‘sleighs”.

2 min TL;DR || Perfect for impressing Your S.O’s Parents

Traditional credit needs reform. “Buy now, pay later” companies are the new kids on the block. Credit is the concept of borrowing money today and repaying it at a later date. Credit serves many purposes. It’s like eating - we may need to consume more than what we can provide ourselves. However, fair credit options have been scarce: the credit card first launched in 1950 yet other options remain limited. Interest rates have increased and the “terms & conditions” sections have grown in complexity. Today, the average American owes $6.2k in credit card debt. At an average 17% APR, this translates to over $1k in interest alone.

It’s oversimplified to say that credit usage is bad or good. Rather it’s about how it’s used and what is available. Sure, people may make poor spending decisions or lack personal finance knowledge. However, blaming these two factors is like taking someone to a dessert shop and admonishing them when they order cake for dinner. Rather, we need healthier options on the menu to choose from. When it comes to credit, the menu historically has consisted of just credit cards and high interest products like layaway or payday loans.

Today, there’s a new page of entrees being added to the carte du jour - new “buy now, pay later” fintech (i.e. financial tech) companies. But they’re not all transparent & honest - some companies will still have late fees & convoluted terms. Lasagna and pizza if you will. Affirm is different. Overall though, these “buy now, pay later” companies are ahem, cashing in, as they reform credit.

Affirm is a fast-growing business that is changing credit for the better. Affirm stands out on the metaphorical financing menu - it’s the healthy salad that still tastes good. Its honest, transparent financing options stand apart from its competitors. Growth rate, unit economics, team, unique product, amount of merchants, acquisition & retention of customers, network effects, and superior risk model are among its attributes.

As a member of the affluent “PayPal Mafia”, Max Levchin didn’t have to work again. Yet, he founded Affirm in 2012 because he wanted financing to be more fair & honest. To make this happen, he recruited top Silicon Valley engineers, data scientists, and other talented individuals. This powerhouse team has created a “buy now, pay later” behemoth - for instance, its machine learning model approves 20% more customers for loans than other competitor products while keeping delinquency rates at one-fifth of a credit card’s. To fund its loans effectively, Affirm has a loan origination system that doesn’t tie up much cash. The growth epitomizes the success of the company - since 2017, it’s grown over 600%. Since 2019, Affirm has grown 93%. Today, Affirm is a global market leader at $500M in revenue with 6.2M customers and 6.5k merchants.

The market is nascent, with plenty of room to grow. Ecommerce is rapidly growing. In just three years, online sales will account for 22% of the nearly $6T retail market in the US. Of all ecommerce sales, it’s estimated that 3% of them will be paid via “buy now, pay later”. This means the 2023 North Americans total addressable market (“TAM”) is ~9x larger than Affirm’s $4.6B in transactions today. Worldwide, the opportunity gets bigger. There are some well-run competitors in the space (AfterPay, Klarna, PayPal Credit, etc) but Affirm has similar growth, and offers a more transparent array of financing options. It also generates one of the highest sales with better margins. Big pond + big fish = lots of room to keep growing.

The stock is a buy, but sense-check the IPO valuation first. A good company and an overvalued market valuation aren’t mutually exclusive. In the long term, I’d list Affirm as a strong “buy” as I am impressed with its growth and the opportunity ahead. Yet, I’d check that the price makes sense before buying, especially if Affirm goes public soon. As seen from Lyft and DoorDash’s recent IPOs, we’re seeing valuation inflators that overstate a company’s valuation. These inflators include a bull market, overexcitement of investors & media by a big-name IPO, and companies going public after growing rapidly during COVID times. In short, it’s not about timing the market. Rather, verify that the valuation at time of “buy” is reasonable.

About This IPO - Valuation, Equity, Timing, Oh My!

IPO Valuation - $10B to $12B is my guess

In Sep 2020, a $500M Series G was raised at a rumored $5B to $7B valuation.

This is based on looking at Afterpay’s valuation & financials plus revenue multiples and trading comps of other tech companies like Stripe & Shopify. 10x to 15x multiples could be justifiable.Price / share - $50 to $60

Extrapolated based on secondary market share pricing.IPO Timing - early 2021

Affirm has just pushed back its IPO date from December 2020. Reasons could include believing it could get a better valuation after seeing DoorDash & Airbnb’s IPOs, price swings in the market after big-name IPOs, delays at the SEC due to the surge in listing requests, & Affirm sorting out its recent PayBright acquisition.

10 min || Deep Dive

A (quick) background of credit

What is Affirm?

Affirm’s strengths

(1) Delinquency rates

(2) Funding capabilities

(3) Merchants

(4) Customers

(5) Network effects

(6) Talent

(7) P&L management

(8) Key partnerships

(9) Unit economics

Affirm’s weaknesses

(1) Peloton

(2 Cross River Bank dependence

(3) Regulation

(4) Competition

(5) Star CEO

(6) Dual-class structure

Competitors

Market size

Final thoughts

What I wish was included in the S-1

Fun facts

Note to readers

A (Quick) Background on Credit

Credit itself can be a good thing. The traditional credit options aren’t good.

Credit is the concept of borrowing money today and repaying at a later date. The concept of credit existed thousands of years ago. In the US, the 1940s saw the boom of American credit mirroring the surge in consumerism after WWII. New stoves sparkled in kitchen corners, televisions flew off the shelves, automobiles peeled off dealership lots. Credit put the cost of pricier purchases within the reach of more Americans - the first credit cards debuted in 1950. Yet, since the 1950s, credit options remain limited (primarily credit cards) while interest rates have increased and fine print sections have grown in length and complexity. Other options such a payday loans charge up to 400% interest! As a result, Americans owe a total of $1T in credit card debt today. They have $121B in credit card interest, $11B in overdraft fees, and $3B in late fees.

Yet, the credit card limits continue to rise - over the past decade, it’s risen 20% to $31k. Credit cards are inherently at odds with doing right by the customer: they make a profit when customers struggle & can’t pay within 30 days. Up to a third of credit card revenue is from late fees. Credit cards charge up to a 27% compound interest rate if customers can’t pay in full.

FICO also creates a circular dilemma. Those who lack credit such as immigrants or younger generations find themselves in this cycle - without history, they can’t get a credit card. Without a credit card, they can’t build credit history. Thus, it seems logical that credit options should approve based on something other than FICO. And of course, once a customer is approved, loan terms should be fair and transparent.

“Buy now, pay later” options offer alternatives to traditional credit. But not all are benevolent.

Honest credit should profit from adding value to a customer rather than profiting off a customer’s mistakes or inability to pay exactly at the 30-day mark.

The last decade has seen a new era of fintech companies. A subset of them are known as “buy now, pay later” companies. When executed fairly as Affirm does, merchants and customers benefit. Merchants love them because they convert customers and increase cart value. Customers love them because they offer clear, fair interest terms with limited fees. But not all of them are so benevolent. More on the companies in this space in the “Competitors” below.

What is Affirm?

Affirm creates honest financial products that offer credit at transparent rates and teach people to manage their finances better by saving better.

Affirm has 4 main products: 3 are credit products and 1 is a high yield savings account.

Point of Sale Financing

Virtual Card aka “Affirm Anywhere”

Split it- No photo as it’s similar to #1Savings Account

Affirm’s Strengths:

Approvals are higher than competitors’. Delinquency rates are even lower than credit card companies’.

According to third party research, Affirm approves 20% more customers than comparable competitors' products. When it comes to the rate that customers miss payments (“delinquency rates”), Affirm’s is one-fifth that of a credit card: it’s at 1.1% while credit cards are at 5.3%. This success can be attributed to the data science team and its machine learning model - with more data and types of data, Affirm’s risk models generate better outcomes in terms of who to approve and how much to approve them for.

Affirm funds the payments in a low-cash way.

Merchants are paid in full at the time of transaction. Yet, customers pay over time. Thus, Affirm had to figure out how to pay the merchants upfront while waiting to recoup the payments over time from the customers. This is a concept known as loan origination. Directly originating (i.e., paying the merchants out of Affirm’s own cash reserves) necessitates that Affirm hold significant amounts of cash on its balance sheet. Due to fiscal regulation, Affirm also would need to have individual state and country licenses to do so. While it does do some of this for control and margin reasons, Affirm uses mostly loan origination banks such as Cross River Banks to conserve cash. Yet it maintains control and consistency of the customer experience by handing most of the servicing requirements. This means that for customer service questions and late payment follow-ups are handled by Affirm rather than these 3rd party originators.

It’s a win-win for merchants.

As more merchants compete for a finite set of customer “eyeballs”, the cost of acquisition (“CAC”) has risen to $1T annually. Current payment solutions (credit cards, Amazon Pay, PayPal, etc) are there to collect payment primarily. To incentivize customers to check-out, merchants have traditionally turned to discounts or promotional gimmicks. As someone who leads marketing & ecommerce at my job, I have seen how time-consuming marketing promo calendars build outs are, how much margin we give up on discounts, and how promos can erode brand equity over time.

Affirm helps acquire & retain customers better. By spreading payments over 1 to 48 months, Affirm increases average cart sizes by 85% and increases purchase conversions rates. Repeat rates also improve by 20%. These repeat rates translate to merchants seeing 2x spend in the second year as the first year by the same customer. Thus, the KPI of LTV / CAC presents a compelling case for merchants.

It’s loved by customers - Affirm’sNPSis 78. Visa’s is 12 and Chase bank is 31.

Unlike other “buy now, pay later” options or credit cards, Affirm delivers on transparent financing terms. If a merchant does not offer 0% APR (46% of them do), Affirm breaks out how much interest will be paid in each loan term (3, 6, 12 months in the below case). Customers are never charged more - no late fees, only simple interest. Additionally, the user experience is superior - its modern design and mobile-optimized experience lends to customer trust & delight. This is important: 54% of Affirm’s customers are millennials & Gen Z. 70% of this demographic report preferring to shop online and 80% regularly shop using a smartphone.

Network effects accelerate Affirm’s growth.

The more merchants that have Affirm as a payment option, the more customers use Affirm. And the more customers use Affirm, the more merchants will want to have Affirm on their site. This creates a flywheel effect that has helped Affirm expand rapidly. Since 2017, it’s grown over 600%. Since last year, Affirm has grown 93%. Today, Affirm is at $500M in revenue and is one of the global market leaders with 6.2M customers and 6.5k merchants.

When I was working there just a few years ago, higher end retailers were reluctant to sign with Affirm for fear that having a “financing option” on their site hurt brand equity and thereby, sales. Now, retailers realize not only is that not the case, but also that Affirm actually increases the number of sales and the amount spent per transaction. Today, retailers like Gucci, rag & bone, Neiman Marcus, & Oscar de la Renta offer Affirm.

The talent alone is something to bet on.

With the rare exception, everyone I worked with at Affirm was impressive. The same caliber as colleagues I worked with on Wall Street. Resumes and the occasional hoodie made it feel like the office could have easily been a top college admissions fair or elite job fair - “Stanford!” “former Marine!” “McKinsey” “Yale!” “LinkedIn” etc. At company wide “all-hands” meetings, Affirmers across the company could, and would, ask hard-hitting questions to exec. But my favorite part? The underlying sense that we were all in this together to make a difference in the world. It was a meeting of the best minds, here to create something special with Max Levchin at the helm.

The P&L shows a healthy company that is growing rapidly.

Revenue - Affirm makes money in diversified ways. It makes money from merchants, customers, affiliates, and servicing the loans originated by its bank. As we see from Uber’s separate Rides & Eats businesses, and from Airbnb’s lodging & Experiences businesses, diversification of revenue is key to weathering whatever business and macro conditions arise.

Expenses & Net loss - From 2019, Affirm almost doubled its revenue to $510M. Yet, it decreased its net loss from $(120)M to $(113)M. They’re not yet profitable, but the path to profitability is there - some illustrative examples (my postulations only) include expanding its licenses to fund more of cash needs itself, becoming a bank, & creating a loyalty program for customers to go to Affirm for their credit needs.

Key partnerships lay the groundwork for expedited growth.

Shopify is the prodigy of the ecommerce website space - it’s the platform on which brands like KKW Beauty, Bombas, and Gymshark build their websites. In fact, it’s the fastest growing ecommerce software. And it just invested in Affirm and signed a three year agreement that Affirm will be Shopify’s exclusive US provider of an installment loan product.

Affirm has also set its sights north to Canada. It just acquired PayBright, one of Canada’s leading “buy now, pay later” providers.

Unit economics are strong.

Customers are charged anywhere from 0% to 30% APR. Merchants are charged an average 11% of the transaction amount. This 1 1% merchant fee is extrapolated by dividing Gross Merchandise Volume of $4.6M by Revenue from Merchants of $510M.

Affirm’s Weaknesses:

Peloton makes up 30% of Affirm’s total revenue.

No other merchant makes anywhere close to this percentage of Affirm’s revenue. The 9 other top merchants make up 7% of Affirm’s revenue.

Such an outsized dependence isn’t ideal. However three points help mitigate this risk relative to Affirm’s long-run prospects: (a) Should Affirm lose its Peloton business, it still has a lot of addressable market to grow into. It’s on an upward trajectory regardless. (b) 30% has been steady from 2019 to now. And Affirm’s revenues have doubled. That means that Affirm is also doubling the rest of the business. (c) Affirm signed a 3 year agreement with Peloton that ends September 2023.

There is heavy dependence on Cross River Bank “CRB”.

The majority of Affirm’s loans are made through CRB. Should the relationship be strained or a regulatory violation happens, having the capital to pay merchants would be an issue. While these are always possibilities, three things make me feel more confident. (a) Affirm is starting to originate more loans with its own capital through its licenses in the US and Canada. (b) CRB has worked with Affirm for 5+ years now. (c) They just signed a 3 year contract.

Fiscal regulation is complex and abundant.

To protect citizens, there is an abundance of financial regulation. This includes federal laws, state laws, county laws, political dynamics, and data privacy regulations. Both Affirm and all of its originating banks are subject to these complex regulations. To best understand and navigate these policies, Affirm’s CEO Max Levchin served on the CFPB, one of the regulating bodies, for a few years.

Only a few companies will survive and the number of competitors are increasing.

There is a lot of room to grow for all “buy now, pay later” companies as ecommerce continues to grow. Yet, there is also a growing laundry list of companies - Klarna, Afterpay, Sezzle, PayPal Credit, Bread, and more. Growth is a double-edged sword. First, this business works off network effects: the more merchants use Affirm, the more customer trust and want to use Affirm. The more customers that use Affirm, the more merchants want to use Affirm. The other side of the coin is that these payment options can’t all continue to exist. One or a few will eat up the market like Uber, Grubhub, & DoorDash have with food delivery. That will likely come years down the round with how much room there is to grow worldwide.

Any change to star CEO Max Levchin’s role would affect Affirm’s stock immensely.

Max Levchin is part of the well-known group known as the PayPal Mafia. This group created PayPal and includes names like Peter Thiel, Elon Musk, and Reid Hoffman. His star power has been helpful in lending credibility and recruiting hundreds of top talent. However, this also means that should he no longer be CEO, there would be a blow to the company’s external perception. Not insurmountable, but more significant than other companies’ CEOs leaving.

Dual-class structures are becoming more common but could pose issues down the line.

Dual-class structures are becoming the norm for big tech companies. This means that there is a special group of Class B shares that are worth a disproportionate amount of voting rights (15:1 in Affirm’s case) versus the regular Class A shares. This structure helps prevent founders and executives from being removed by external parties like activist hedge funds buying up shares. However, if a company’s executive isn’t doing a good job in the future, dual-class structures make it more difficult to oust them. A shade of this situation happened at WeWork. Still, not at all a big concern for me given company growth. Also, I’ve been in meetings with Max and seen just how strong of a CEO he is (sort of intimidatingly so, if I’m honest).

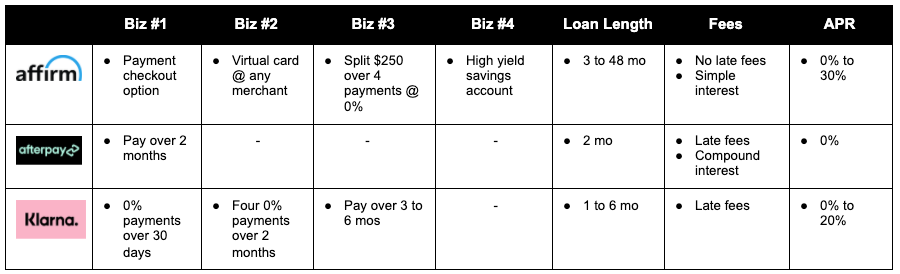

Competitors:

There is industry-wide awareness that new financing options are needed. The list is growing longer - Affirm, Klarna, Afterpay, Sezzle, PayPal Credit, Quadpay, Bread, Zippay, Splitit, Latitude, and more. Affirm, Klarna, & Afterpay lead the pack.

Klarna is the largest but Affirm has top-notch margins. Plus, it’s in the least amount of countries and yet is still similar to Afterpay’s revenue. It’s a race though, and I’d personally be putting my bets on all three right now. There’s plenty of white space for everyone but I’d keep an eye on market share.

Business models of the top 3:

Results of the top 3:

Size of Market:

There is a lot of room to grow into. In the next 3 years, “buy now, pay later” transaction could account for almost $1T of ecommerce spend between North America, Europe, the Middle East, and Africa.

North American “Buy Now, Pay Later” market size in 2023

$5.8T that is the US + Canada retail market in 2023

x 22% of retail that will be online sales

= $1.3T in North American ecommerce sales

x 3% of all ecommerce sales

⇒ $39B

EMEA “Buy Now, Pay Later” market size in 2023

x 10% of all ecommerce sales

⇒ $60B

Some Final Thoughts

What I Wish Was Included

Customer cohort behavior - this includes average order value, churn rates, and overall repeat rates. Customer cohorts are essential performance metrics to track for any business

Total addressable market breakdown - Affirm’s S-1 talks about market size of ecommerce relative to retail and what % “buy now, pay later” is in the US, but not internationally in every region

More years of financial data pre 2018

Details into expansion into Canada & internationally - Canada is a big focus given its recent acquisition of PayBright. Would have loved thoughts on where Affirm sees itself going but understand the want to keep mum. The competition is heating up in this space

Fun Facts

A growth story, told by the # of offices - I was at Affirm for about two years. During that time, we moved three times because we were growing so fast. It went from a single floor, to a few floors, to whole wings & sections of a huge downtown FiDi San Francisco building

Meeting rooms with thematic names - at the first building we were at, the meeting rooms had coffee names: “ristretto”, “americano”, etc. At another one, they had plant names “maple”, “oak”, “poplar”. Because we kept switching offices, it felt a bit like Hogwarts for a period - always trying to figure out where your next meeting room was located

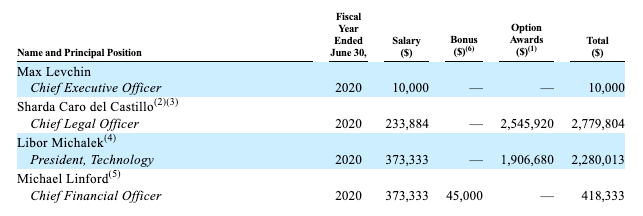

Exec compensation

Financial disclaimer: On all investments, please do your own research. I am not a financial advisor and opinions are my own. All information referenced is publicly available.

Finally, thank you - a special shoutout to my friends Emily Allbritten (@eallbritten), Sam Parr (@thesamparr), & Sara Sodine (@sarasodineparr) + my other wonderful friends & amazing people I’ve met through my newsletter and Twitter. Your support & constructive feedback truly mean the world. Thank you so much for allowing me to nerd out on topics I love & share them by “writing in public”. It’s exciting, daunting, and humbling all at once.

Folks loosely throw around the data point of average American having $6.2k of credit card debt.

What’s the median? What % of income is $6.2k? Does this include business credit debt?

Digging into the data suggests the median # is about 50% of $6.2k. This makes me think business loans are included in that figure causing an increased average.

Further, average credit debt rises with average income.

I hypothesize that the current credit model isn’t nearly as broken as these numbers suggest.